Last Thursday, Apple announced its Q4 FY2022 earnings results as follows

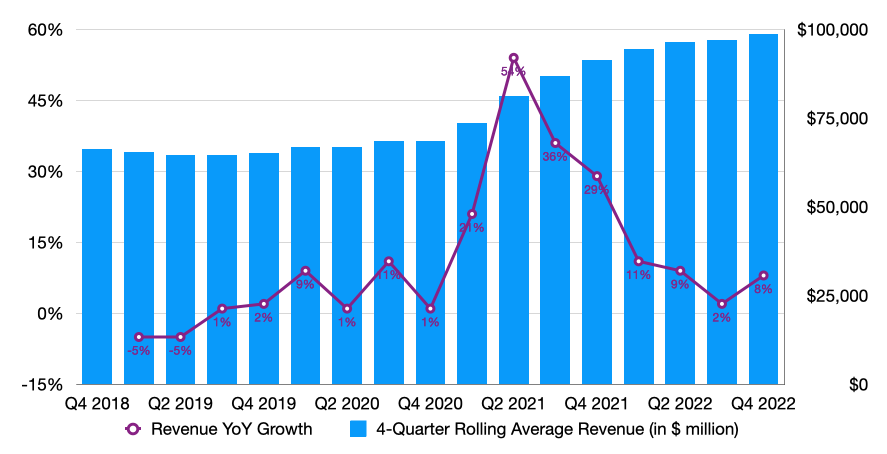

- Revenue: $90.15 bn vs $88.9 bn estimated. Up 8% year over year (YoY)

- Gross Margin: 42.3% vs 42.1% estimated. Essentially flat YoY

- iPhone revenue: $42.63 bn vs $43.21 bn estimated. Up 9.7% YoY

- Mac revenue: $11.51 bn vs $9.36 bn estimated . Up 25.4% YoY

- iPad revenue: $7.17 bn vs $7.94 bn estimated. Down 13.6% YoY

- Other Products revenue: $9.65 bn vs $9.17 bn estimated. Up 9.9% YoY

- Services revenue: $19.19 bn vs $20.1 bn estimated. Up 5% YoY

- EPS: $1.29 vs. $1.27 estimated

On the surface, it looks like a routinely great quarter for Apple, but there are a few points worth calling out.

First, Apple got hit with a 600 basis point of unfavorable foreign exchange impact due to the strength of the dollar. Had the currency exchange stayed constant, Apple’s revenue growth would likely have been two-digits and could have gone up to as much as 14%. Despite significant foreign exchange headwinds, product margin was 35%, flat compared to Q3 FY2022, and 100 basis point up year over year. This indicates Apple managed to gain efficiency and sell more expensive products. To investors who care about how a company is run, this is a good sign.

Second, the stickiness of iPhone. Since Q4 FY2020, iPhone revenue has increased year over year every quarter. In FY2022, iPhone revenue grew by 7%, on top of the monstrous 39% growth achieved in FY2021. As a billion business worth more than $200 billion, that’s no mean feat. More impressively, the numbers could have been even rosier. According to Tim Cook, the company has been facing and still faces supply chain constraints for the popular iPhone 14, iPhone 14 Pro and iPhone 14 Pro Max. Had Apple had enough parts to meet the demand, they could have added a couple of more billions to their top line. In the time of unprecedented inflation and uncertain macro-economic conditions, this shows how much consumers love their iPhone and considers it more of a necessity than a luxury.

Next, Services grew 5% YoY and slightly missed analysts’ expectation. Adding the estimated foreign exchange impact of 600 basis points, Services would have grown by 11%, beating the consensus. Since 2018, Services has grown by double digits every year, reaching $78.1 billion in annual revenue in FY2022, up from almost $40 billion in 2018. Compared to previous year, FY2022 posed a lower annual growth, but there are levers that Apple can pull:

- Apple recently announced price hikes on Apple Music, Apple TV+ & Apple One. The company explained that the price increase for Apple Music is due to more payouts to artists while that for Apple TV+ is fair considering the amount of content that Apple has added since the launch of the streaming service. As the flagship overarching subscription, of course, Apple One will also be more expensive. I think the justification makes sense because if Apple REALLY wanted to increase Services revenue and abuse its power, the company would raise iCloud’s prices. There are alternatives to Apple Music and TV+, but there is nothing to replace iCloud and no Apple user I know doesn’t buy additional storage. In short, this is not a move out of desperation.

- Apple is loading more ads on the App Store. In their 2022 annual report, the company already cited advertising as one of the main drivers behind Services’ growth. Ads revenue is great and all, but too many ads will harm the user experience. Plus, there is already backlash from developers who saw online gaming ads placed next to their apps. Hence, Apple needs to be careful and considerate about pushing their advertising division

- Apple Business Essentials. There has been no disclosure from Apple regarding this service, but I suspect it will come to the fold more in the next couple of years

Last but not least, I am really pleased with how Apple manages its costs. The gross margin profile of Products, Services and the whole company have been very stable in the last four years, despite Covid-19, the war in Ukraine, the withdrawal from Russia, the supply chain challenges and other macro-economic events. Operating expenses, including R&D and SG&A, as % of total revenue never exceeded 8% in the last four years. Based on the commentary from the executives, that should be the case for the next twelve months:

When we look at our capex, as you correctly said, I mean, we’ve been fairly stable, and I think our capital intensity is really very good. We have three major buckets in capex for the company. We have certain dedicated tools for the manufacturing facilities. We had some spend around data centers, and we have spent around our office facilities around the world. We obviously monitor all of them. There is nothing unusual that we see for the next 12 months.

When a company reaches a trillion dollar mark in valuation and generates billions of dollars in cash flow every 90 days, there is understandably a risk of being negligent on cost control. Think about yourself. Do you allow yourself more luxuries and impulsive purchases now than you did as a student and when you had lower income? From this perspective, Apple has been a disciplined and prudent steward of shareholder capital. To some extent, I don’t think you can make the same point about other big techs, such as Amazon or Facebook.

In short, this quarter’s results were not the most impressive that Apple has ever put out. They were just routinely and boringly good from my perspective and for the reasons I listed above. Even though there is no headline-grabbing debate-fueling stuff such as the investment in Reality Labs by Facebook, I prefer a stable and effective management that keeps their feet on the ground and produces results for shareholders.

Leave a comment