On that FY2019 Q2 earnings by Amazon…

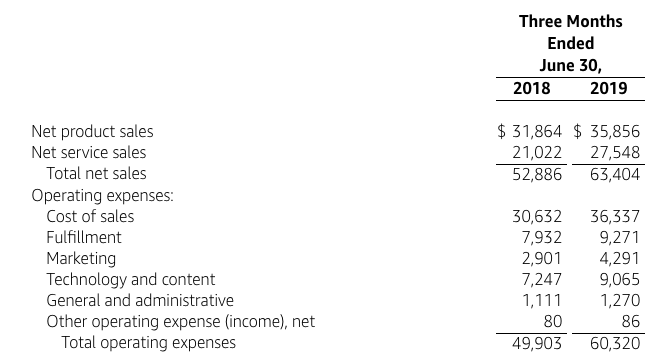

Revenue

In the last 90 days, Amazon recorded $63 billion, meaning that it took the company less than 36 hours to make $1billion. An extraordinary rate. Compared to last year’s Q2, revenue rose by 20% with Services (31%) outperforming Products (12.5%). Nonetheless, gross margin slipped as this quarter’s figure is at 4.8% compared to 5.6% last year.

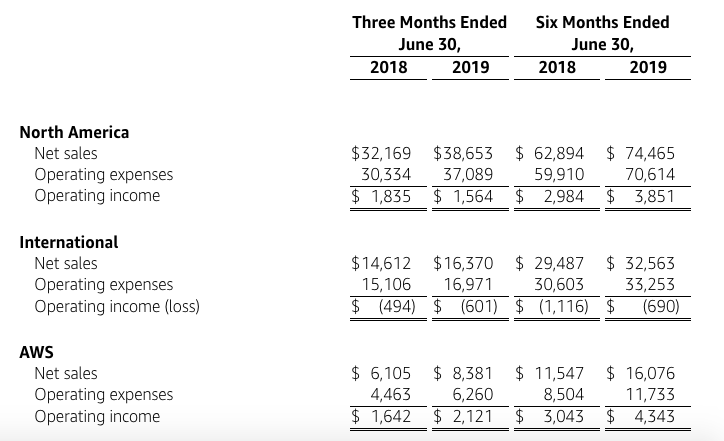

AWS

Among Domestic, International and AWS categories, the latter continues to lead the way in terms of YoY growth. AWS’s revenue in the last 90 days is $8.3 billion, a rough equivalent of about $32 billion annually. It’s pretty impressive for just a segment of a company. Not many standalone companies can generate that much revenue in a quarter. It’s even more telling when we put AWS next to GCP. Google announced last week that GCP’s annual run rate is $8 billion, meaning that AWS is approximately 4 times bigger than its rival from Google.

Despite making up only 13% of Amazon’s revenue, AWS is responsible for about 69% of the company’s operating income.

At 37%, AWS’ YOY growth is the lowest recorded in a long time, but the law of big numbers should be taken in account here as the division is not as small as it used to be. If broken down into more strategic categories, AWS isn’t the segment with the biggest YoY growth (Excluding FX) in the company. It’s Subscriptions. Subscription memberships, especially Prime, play a crucial role in Amazon’s ecosystem. The fact that it notched the biggest growth, ahead of AWS, is very positive for the company.

Advertising

As can be seen above, advertising slowed down significantly after a hot streak just 12-15 months ago. YoY growth decreased noticeably compared to the 3-digit growth just a while ago. Still, it contributed $3 billion to the company’s top line.

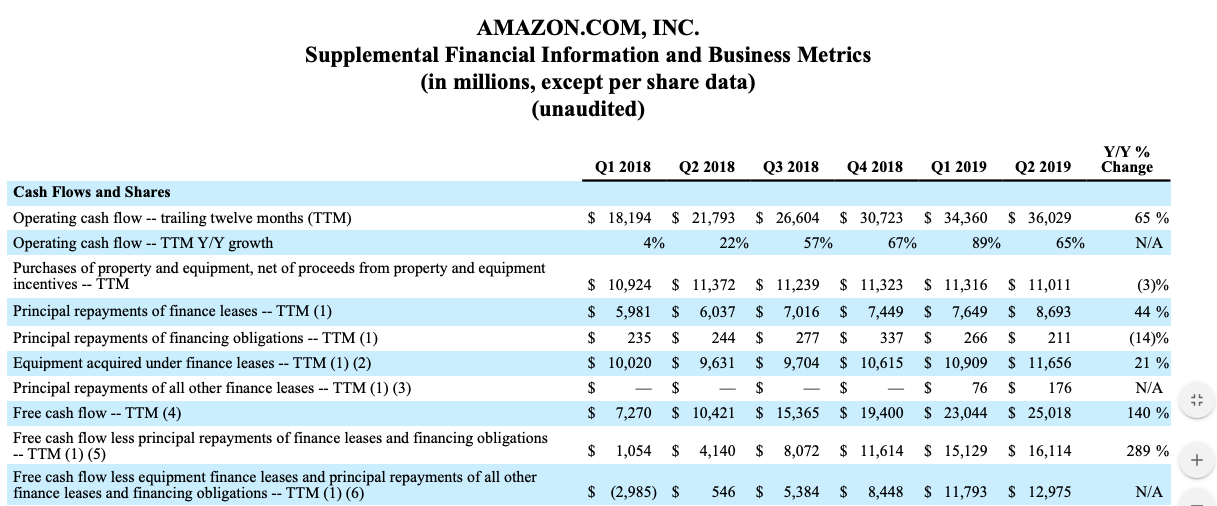

Free Cash Flow and Shipping Costs

Amazon’s free cash flow this quarter is truly insane with 65% YoY improvement in Operating Cash Flow and a 3-digit growth in Free Cash Flow.

Shipping costs continued to rise with 36% YoY difference compared to previous second quarter’s. It’s worth noting that none of the Online Stores, Physical Stores and 3rd Party Seller Services have the same growth (all grew at a slow pace than shipping costs)

Sometimes, it’s hard to believe that a company founded roughly 25 years ago can be this powerful and big. A segment responsible for only 13% of its revenue is the dream of so many and it continues to deliver at an impressive rate.

Leave a comment