A bullish argument for money-losing companies (companies that have negative operating income) I have seen so far is that they are following the footsteps of Amazon in the early 2000s before the juggernaut became what it is today. Set aside the differences in business environments, the nature of industries and technological advances, there is one important caveat; even though Amazon reported negative net income for a few years before turning profitable, it had POSITIVE free cash flow during that time.

Per corporatefinanceinstitute, Free Cash Flow (FCF) “represents the amount of cash generated by a business, after accounting for reinvestment in non-current capital assets by the company”. It’s equal to, simply speaking, cash generated from operations minus Capital Expenditure (CAPEX). It is a metric to show investors how efficient a company is generating cash and whether the company at hand has enough to pay investors after operational needs and capital expenditures.

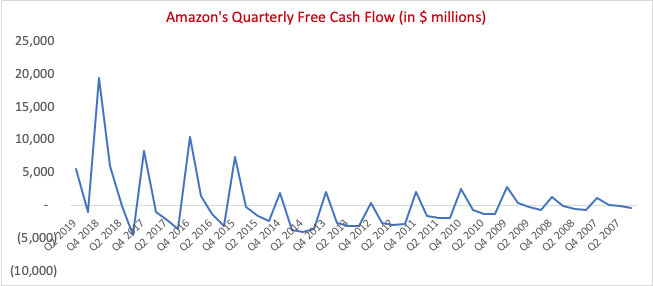

This is what Amazon’s annual and quarterly free cash flow looks like over the years. Data is from macrotrends:

Over the years, free cash flow noticeably grew bigger for Amazon, but it was positive even before the introduction of AWS in 2006, which has been the margin maker for Amazon recently. Hence, if a company has negative operating income and still makes capital expenditures to grow, they are NOT similar to Amazon.

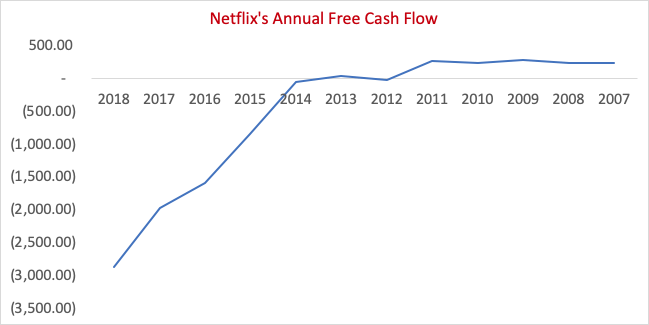

A particularly intriguing case is Netflix. The streaming king debuted its streaming service in 2007 and has grown to become the de facto leader in the market. It has had positive operating income, but increasingly invested a massive amount of money in original content, much more than the cash it generates from operations every year.

Since Q3 2014, Netflix hasn’t had a single quarter with positive FCF. The challenge Netflix is facing compared to its competitors is that Netflix has only one source of revenue. Disney, Amazon and Apple, to name just three competitors, have different sources of income. In the case of Amazon and Apple, their streaming services can be argued to be add-on services that function to lock in customers. It is true that given its almost 150 million subscribers, Netflix can spread its content costs across more subscribers than its competitors. Nonetheless, it has to keep investing every year in original content to appeal to consumers. If there is no change in how Netflix can generate revenue besides subscription, I struggle to see how its FCF outlook will differ. Hence, Netflix’s story is NOT similar to Amazon’s in the early 2000s.

Leave a comment