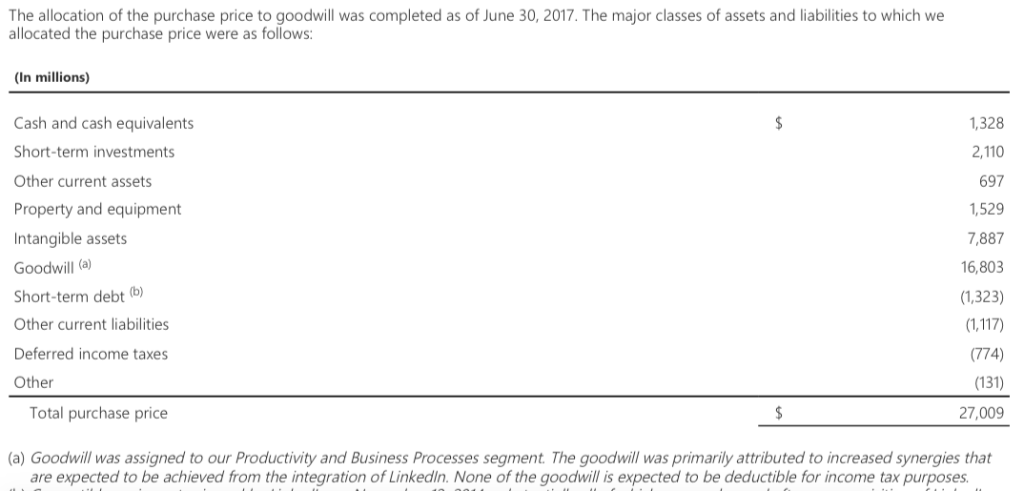

In December of 2016, Microsoft paid $27 billion in total for LinkedIn and completed the acquisition. According to the latest annual report, the majority of the acquisition price came from goodwill which Microsoft clarified as primarily synergies gained from the integration of the acquired social network.

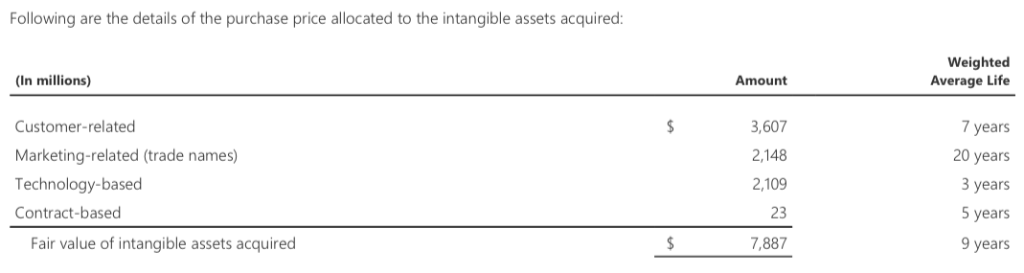

Interestingly, among intangible assets, Microsoft assigned a little more than $2 billion for the trade names. I am not entirely sure whether it means Microsoft valued LinkedIn’s brand as that price. There seems to be a difference between the two concepts: trade names and trademarks, even though in some cases, the two can be interchangeable.

Apparently, during the fiscal year when the acquisition took place, LinkedIn generated $2.2 billion in revenue, but registered a negative operating income

Fast forward two years later, LinkedIn increased its revenue by almost 200%, from $2.2 billion to $6.7 billion approximately

In terms of members, LinkedIn had 500 million members, 575, 645 and 660 in 2017, 2018, 2019 and Q1 2020 respectively. It’s interesting to notice how Microsoft commented on the primary source of revenue from LinkedIn. LinkedIn’s lines of business include Talent Solutions, Marketing Solutions, and Premium Subscriptions. As of the quarter ended December 31, 2017, most of LinkedIn’s revenue came from Talent Solutions

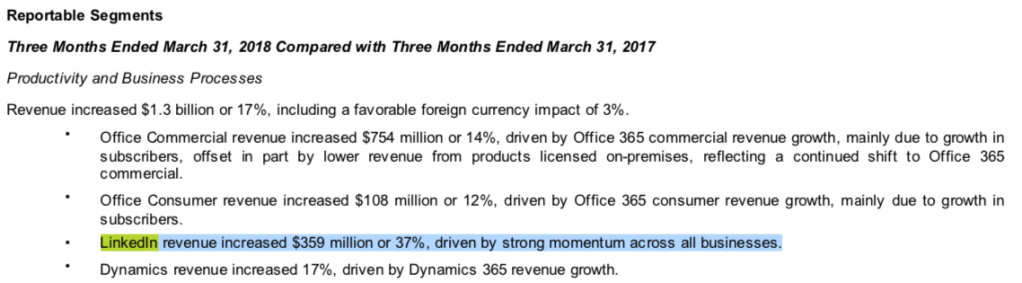

Since the quarter ended March 31, 2018, Microsoft didn’t make such a comment any more. Instead, it has been replaced with “strong momentum across all businesses” or something along that line

It is not clear whether all lines of LinkedIn’s businesses contribute meaningful revenue now. Given the explosive growth in revenue, it won’t be surprising if that’s the case. After all, multiple firing cylinders are better than one.

Disclosure: I own Microsoft stocks in my personal portfolio

Leave a comment