A few days ago, Amazon released the results of their Q1 FY2021 and did not disappoint. You can find their results here. Below are some of my takeaways and charts for illustration purposes

A growing giant

This is the first quarter where Amazon’s average 4-quarter rolling net sales exceeded $100 billion. Think about the scale for a month. In other words, for the past 365 days, Amazon generated more than $1 billion per day on average. What’s more impressive is that their YoY growth has been on an upward trajectory for the past few quarters, hitting 44% in the recently reported one. That’s the kind of growth you often see at companies at a much smaller scale, not a company that is well on track to produce half a trillion dollars in sales a year.

I don’t know where their next growth will come from and that may be the scary thing about this behemoth

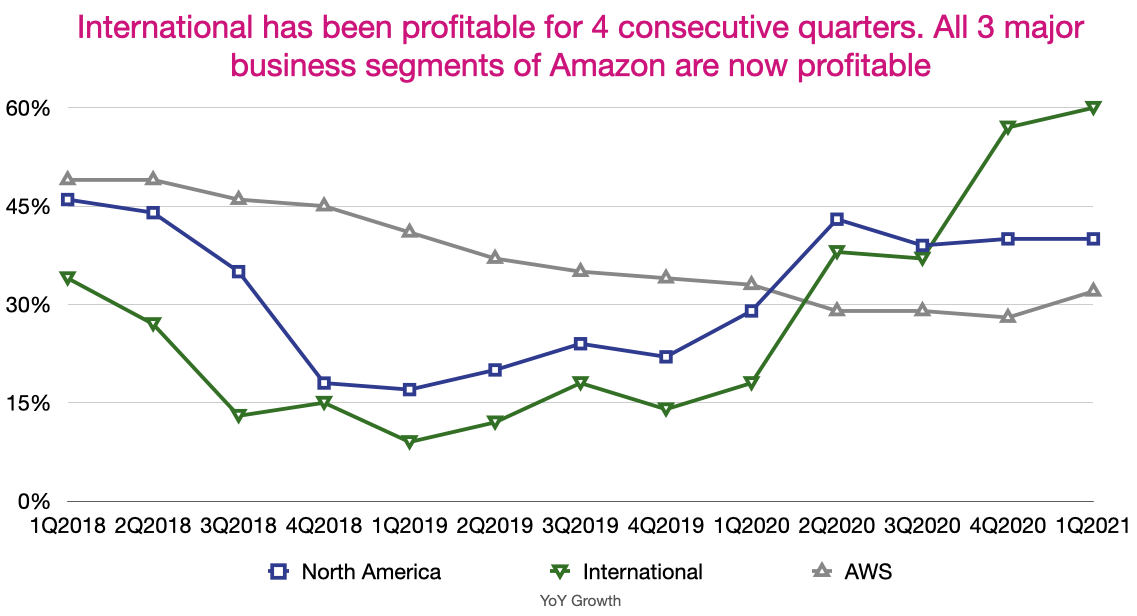

Among the three main segments, North America is the biggest in net sales, almost double the combined figures from AWS and International. Bewilderingly, it has been growing at a higher clip than AWS in the past four quarters, lacking behind International, whose YoY growth just hit an astounding 60% in this quarter. If you look at the segments’ size, their growth figures and growth trajectory, it’s not straightforward to say which one will drive Amazon’s growth in the future. If Amazon can crack the Grocery and Last-Mile code in the US, it will be huge for their North America numbers. In terms of International, there is still a lot more to gain. Take Vietnam as an example. My country’s retail market is huge and growing fast. Yet, there is no such equivalent of Amazon. There are indeed big players such as Shopee, Tiki or Lazada, but they are eCommerce players and the breadth of their offerings isn’t as extensive as what Amazon can offer. Plus, if you ever try the apps of these companies, you’ll chuckle and say to yourself: if somebody can offer a better shopping experience, there is a lot of money to be made here. Lastly, global companies are going through digital transformation, a trend that is accelerated by Covid. It’ll be a boon to AWS’ business.

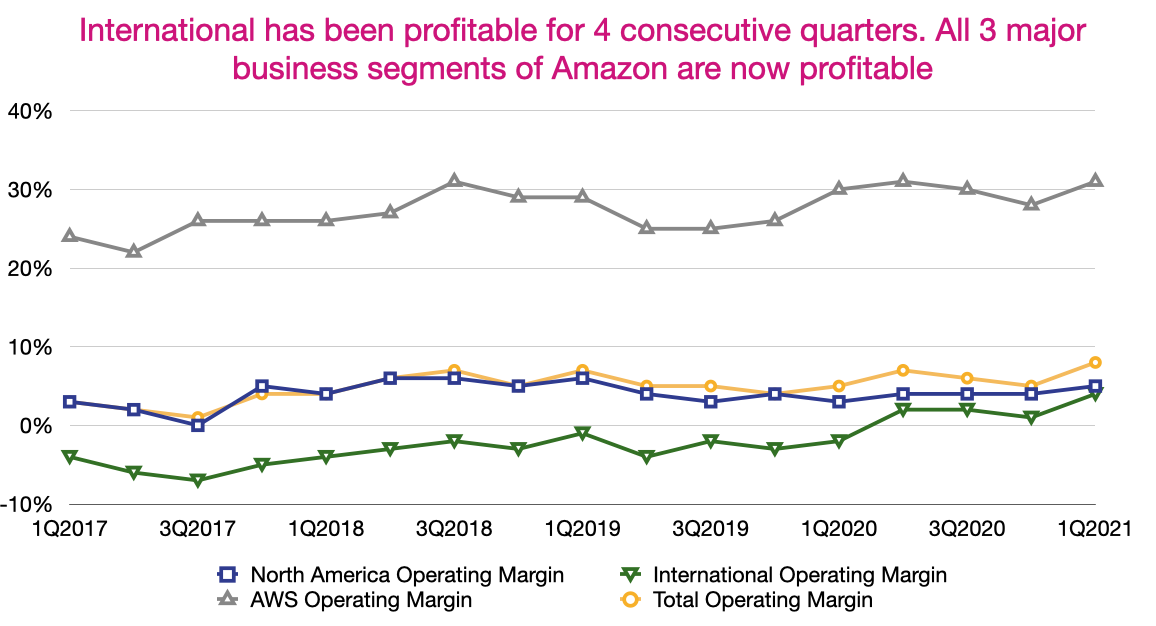

There are bull cases to make for each of these segments. I honestly cannot tell where the next growth will come from. Not because there isn’t. But because there are more than one obvious answer. For good measure, all three are now profitable. International used to be the black sheep, but it has been profitable for the past four quarters.

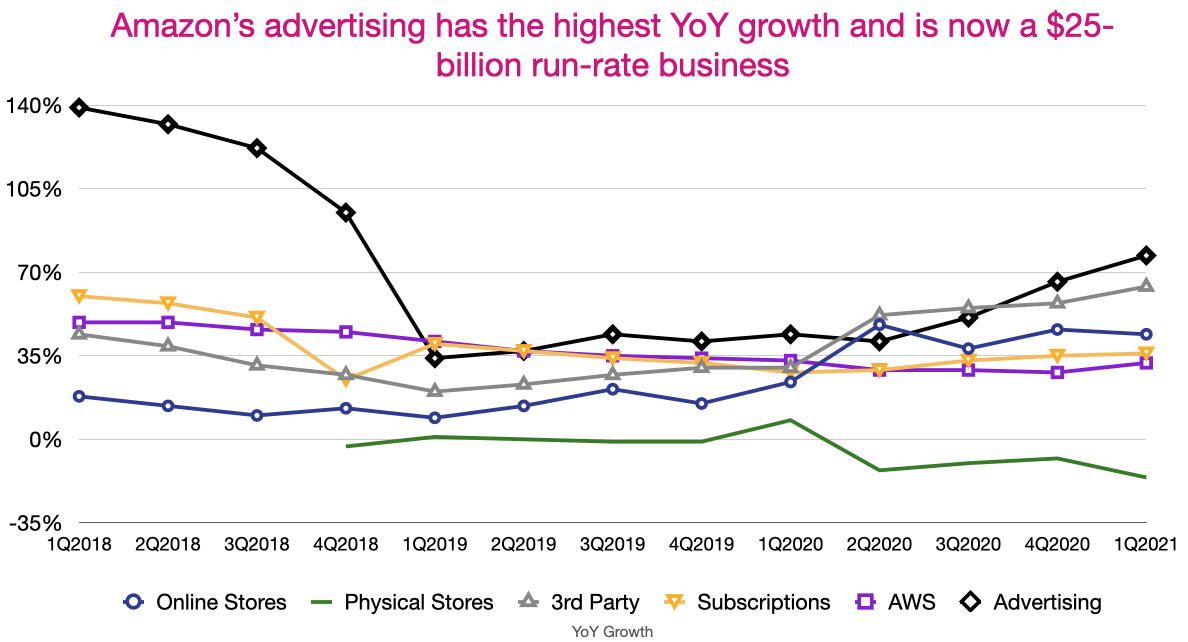

Advertising and 3rd party are growing fast, but don’t sleep on physical stores

Among the business lines, 3rd party and advertising, both high-margin, were the fastest growing with the former growing at 64% YoY and the latter at 70% in this quarter. At $80 billion annual run-rate, 3rd party is highly impressive, growing at 64% YoY. Amazon doesn’t break down 3rd party for domestic and international markets, but it’s not strange to think that as Amazon gains foothold in more overseas markets, more merchants will want to get on the platform. Meanwhile, advertising almost reaches a run rate of $25 billion, growing 4x in the last 3 years. Impressive as it is, there is still plenty of room to grow, both domestically and internationally. As Amazon’s online stores attract millions of buyers, advertisers will be interested in promoting their products or services on a platform where the intention to buy is high.

Even though physical stores’ growth doesn’t look particularly great, don’t sleep on them. Physical stores were first reported by Amazon in 2017. They are relatively new and I consider them strategic investments from the company. Amazon will not be able to compete with Walmart in groceries’ scale and the network of stores as well as fulfillment centers across the country. Hence, they will likely use technology and efficiency in delivery as competitive advantages. Hard to pull off, cashierless stores will save Amazon on personnel costs and provide a differentiated shopping experience for customers. They may also play a role in Amazon’s network of middle and last mile delivery. Eventually, customers may still receive cheaper groceries from Walmart, but some may be more interested in a different shopping experience and expedited delivery from Amazon.

In the United States, we’re delivering out of our Whole Foods stores, and we’ve engaged — we’ll be allowed to pick up a greater expansion of pickup at Whole Foods stores. Amazon Fresh became a free Prime benefit, as you know, in the late part of 2019. And customers really adopted it and continue to see strong growth. So I think on the fresh stores, it’s a little too early. The stores themselves, we’re confident that the Just Walk Out technology that will be a boon, a benefit to customers.

Source: Amazon’s CFO from Q1 FY 2021 Earnings Call

Leave a comment