There are two main stories regarding Disney: Disney+ as well as other streaming services and their non-streaming segment.

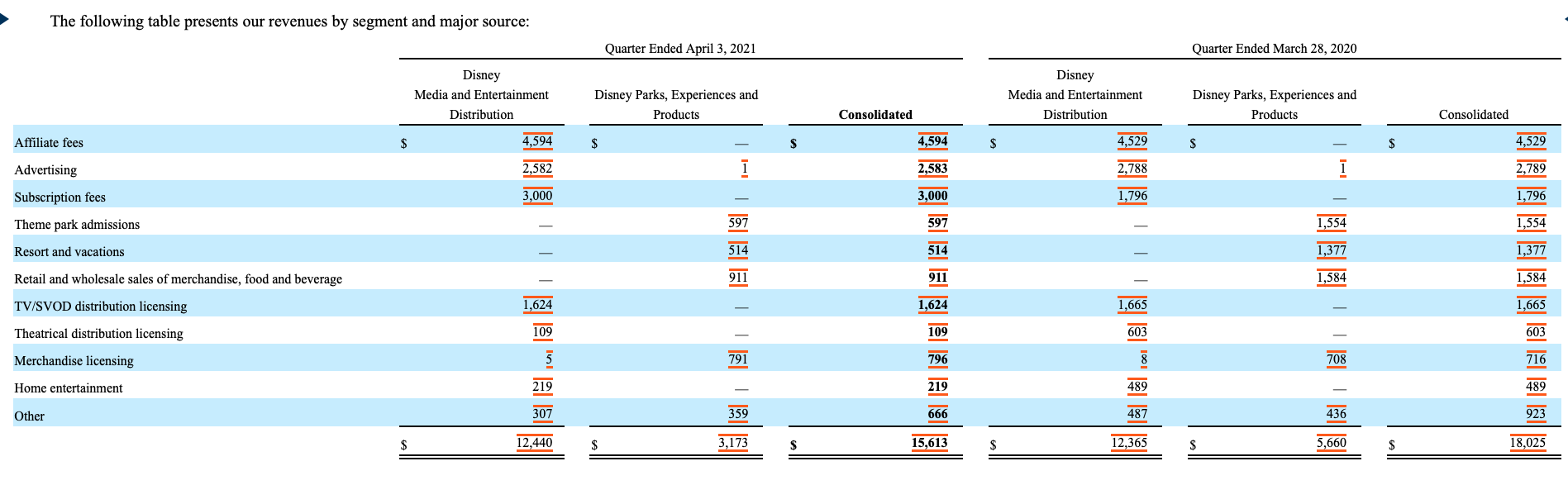

As more and more folks in the US are vaccinated and the CDC relaxed its guidelines, Disney reopened its theme parks and resorts in the last quarter. Traditionally, this segment is the key source of Disney’s profit, but was severely hit by Covid-19. Compared to the prior year quarter, Q2 FY2021 saw revenue from Parks, Resorts, Cruise and Merchandise drop by more than 50%.

Hence, having their physical attractions open is definitely good news to investors. It’s also a testament to the resiliency and health of the business. Its cash cow was hit very hard by the catastrophe that is Covid-19, yet it pivoted successfully to Direct-to-Consumer while waiting for better days to come. In addition, Disney is going to launch an all-new Avengers campus in California on June 4 and allow bookings for its new cruise ship Disney Wish starting May 27th. The Avengers campus, I suspect, will be a big hit to consumers. Thousands, if not millions, love the 10 year story arc with about 23 Marvel movies. As the original cast such as Chris Evans or Robert Downey Jr is more or less out of the picture and the new generation of superheroes are slowly making their way to the scene, fans will cherish a chance to connect physically with their old and new heroes. That’s the power of Disney. They invest a lot of money in creating content and then luring consumers to visit their parks, resorts, cruise lines and buy merchandise. While other streamers can compete with this company on the content front, few, if not none, have the capability and resources to replicate what Disney has on the other part of the equation.

Disney’s Streaming Services

Because Disney+ is touted as the company’s single most important priority, all attention is fixated on the health of the service. At the end of Q2 FY2021, Disney+ has almost 104 million paid subscribers, up from 95 million in the previous quarter. The net add of 8.7 million paid subscribers is much lower than what Disney added in the previous three quarters during Covid. The executives blamed the following for the smaller add:

- Covid pulled forward subscribers

- A price increase in two main markets: EMEA and North America

- No new market launch. The launch of STAR+ in Latin America is postponed to the end of August to leverage major sports events such as the new season of Premier League, La Liga & Copa Libertadores

- A disrupted schedule of Indian Premier League, India’s national cricket league

On the earnings call, the company reaffirmed its target of 240-260 million paid subscribers on Disney+ at the end of fiscal year 2024. To meet the lower end of that target, by my calculation, Disney needs to have a net add of about 12.5 million subscribers every quarter between now and Q4 FY2024. As you can see above, there are quite a lot of factors that can affect the number of subscribers, but if I have to make a bet, I’ll say that they can do it. There are two reasons. The first one is that Disney+ right now is only available in 31 countries. It’s not even live yet in Asian or LATAM countries where there are a lot of folks. My country alone has 96 million people and 50% of those are between 18 and 54 years of age. There are a lot of spots on the world map where Disney+ can expand its presence. The second reason is that the company lowballed their subscriber target before. It’s likely that they may be doing it again with the current one.

The main criticism of Disney’s current growth strategy is that it relies too much on the low ARPU market in India. Hotstar makes up 1/3 of Disney+ total subscriber base, up from 25% two quarters ago. The low price in India suppressed ARPU of Disney+ from $5.61, excluding Hotstar, to just $3.99, including Hotstar. While ARPU is obviously an important part of a streaming business, it’s equally important to take into account where Disney+ is at the moment. Fans of Netflix usually cite its scale as the main competitive advantage. In other words, Netflix has a cost advantage because it can spread content expenses over many more subscribers (around 200+ million). To negate that advantage of Netflix, Disney+ has to grow its base, but it would need a magic wand to acquire more users and grow ARPU because that’d be virtually impossible.

Any comparison between Netflix and Disney+ at this stage is very challenging. First of all, Netflix is available in 190+ countries whereas Disney+ is only in 31. When Netflix started, the category didn’t exist and it had to be a trailblazer. But it also means that Netflix didn’t have a fierce competitor like its current version nowadays. Any price it set was essentially the best price at the moment. On the other hand, while Disney+ doesn’t have to create a whole new market like Netflix did, it has to compete against an established and experienced rival that has a major cost advantage. There is a vicious cycle at play here. Netflix’s competitors have a cost disadvantage because they have a smaller scale. The longer that disadvantage persists, the hard it is to plow billions of dollars a year into content. Without content, there wouldn’t be any subscribers, hence, Netflix’s advantage is reaffirmed. As a result, the likes of Disney+ have to prioritize scale over ARPU for the time being, to avoid being sucked into that vicious cycle. Another difficulty lies in the different operating models. Netflix’s content is rarely available in theaters. Its content library is available to all subscribers without restrictions. Meanwhile, Disney+ releases its content in different fashion:

- Exclusively available to all subscribers without additional charge

- Exclusively available to subscribers with Premier Access (about $30 per title) for a few weeks before being widely available to all

- Available first in theaters for a period of time (45 to 90 days) before going to Disney+

The variety in the release strategy may affect the user acquisition to Disney+, compared to Netflix, but who is to say that it doesn’t help Disney generate more money or profit from taking a different path? Disney+ tried the Premier Access with Wulan and a couple of movies afterwards. I reckon that it must have yielded some success so that they decide to keep it moving forward. With an exclusive theater period, Disney is trying to see if the high margin revenue from theater owners are worth suppressing the subscriber base on its flagship streamer. Whether the flexible model employed by the iconic brand or the dedicated philosophy of Netflix will prevail remains to be seen.

Besides Disney+, I am excited about ESPN+. The service has been growing very nicely in terms of subscriber count and ARPU. At 13.8 million subscribers, there is still a lot of upside within the US to go. For sports fans, its content library is very appealing with Serie A, Bundesliga, UFC, Australian Open, US Open, Wimbledon, MLS & College Basketball. The new deals with Major League Baseball to stream 30 games per season till 2028 and with La Liga in an 8-year deal to stream 300+ matches per year in both English and Spanish will absolutely make it more attractive. Since streaming rights need to be negotiated for every geography, it remains to be seen how or if Disney is able to grow ESPN+ out of the US.

Leave a comment