On Thursday, Amazon released their Q2 FY 2020 results and it was nothing short of impressive. Below are my notes:

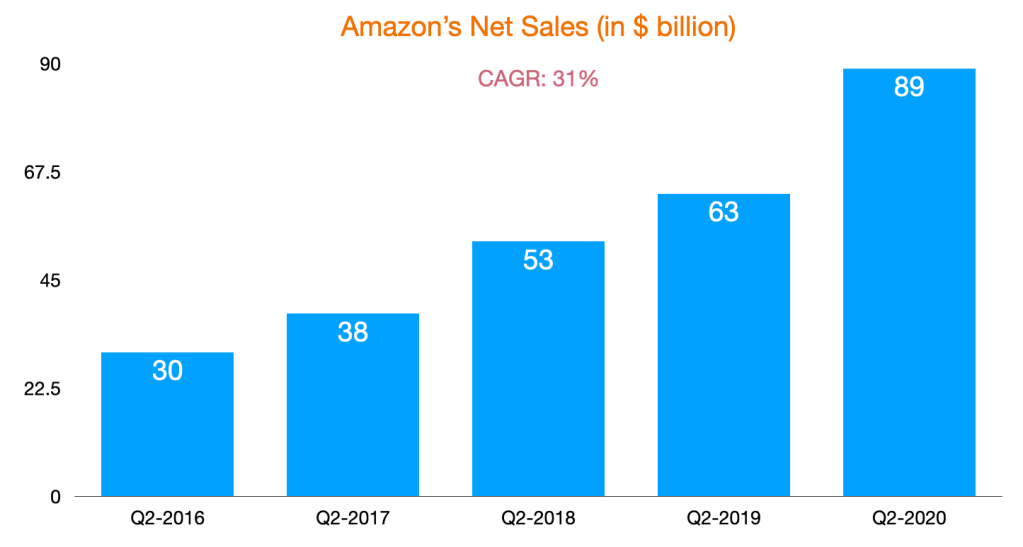

Even during the pandemic, Amazon net sales were $89 billion in Q2, up 40% YoY. In fact, if you look at their net sales in Q2 in the last 5 years, it’s an astounding 31% CAGR.

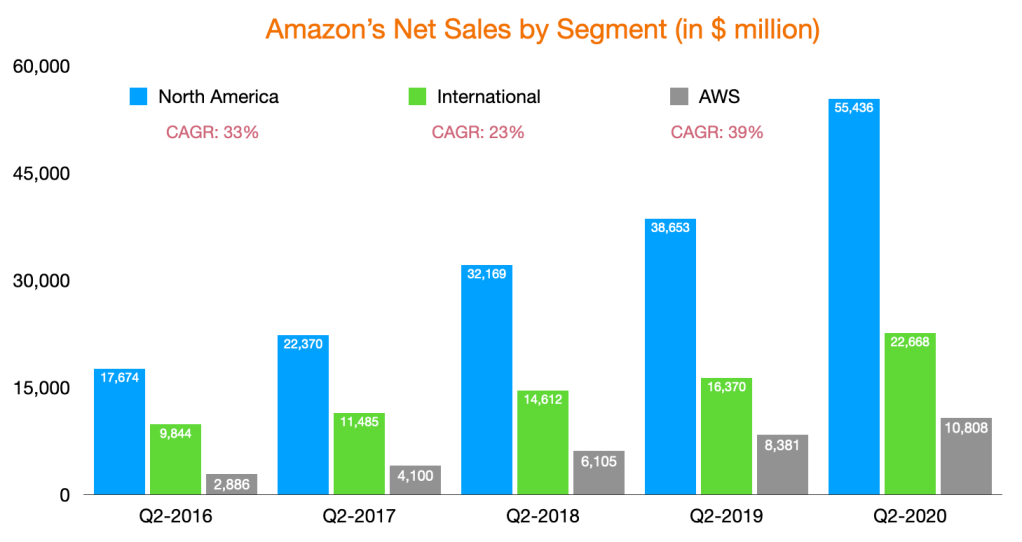

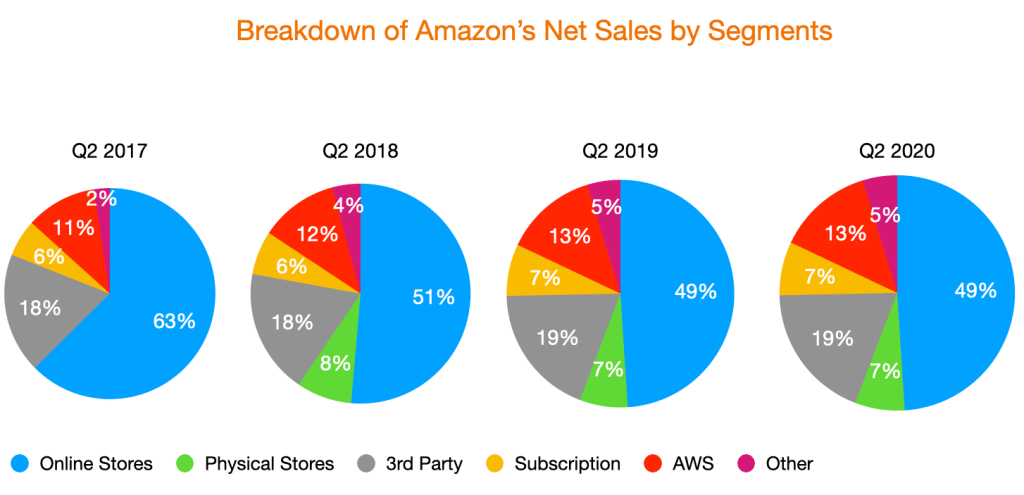

North America still led the way among their three main segments with more than $55 billion in net sales. AWS is now an annualized $43 billion business and responsible for 13% of Amazon’s total net sales. In the last 5 years, CAGR for North America, International and AWS is 33%, 23% and 39%! If you look at a deeper level, online stores were still responsible for the bulk of Amazon’s net sales while 3rd party and AWS were the next two largest segments. Advertising accounted for 5% of Amazon’s net sales. Their shares have stayed largely the same for the past 3 years,

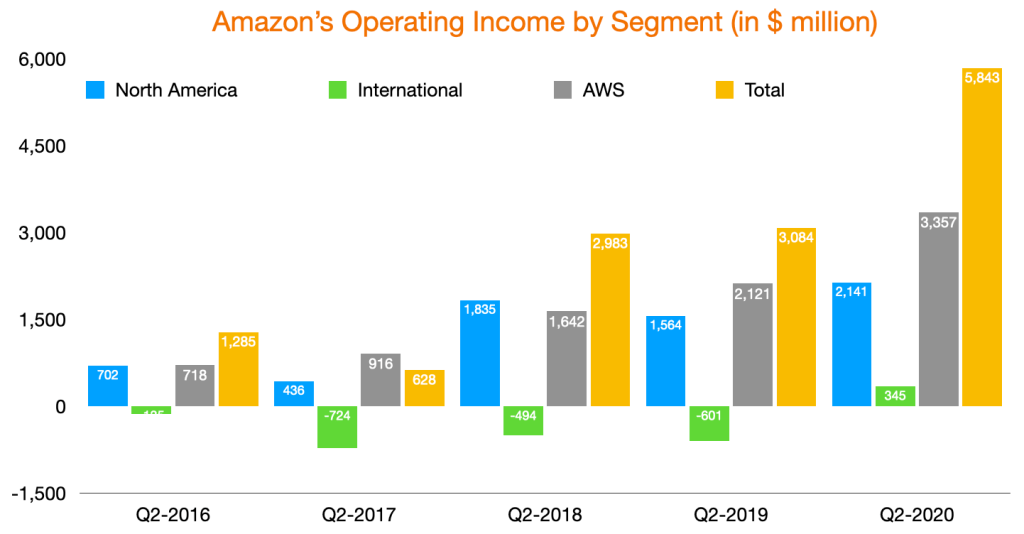

AWS continued to account for more than half of Amazon’s operating income. Historically, Amazon lost money on their International front, but in this quarter, the segment recorded $345 million in Operating Income. Total operating income was up to more than $5.8 billion, almost up by 90% YoY. Once again, this was during a pandemic.

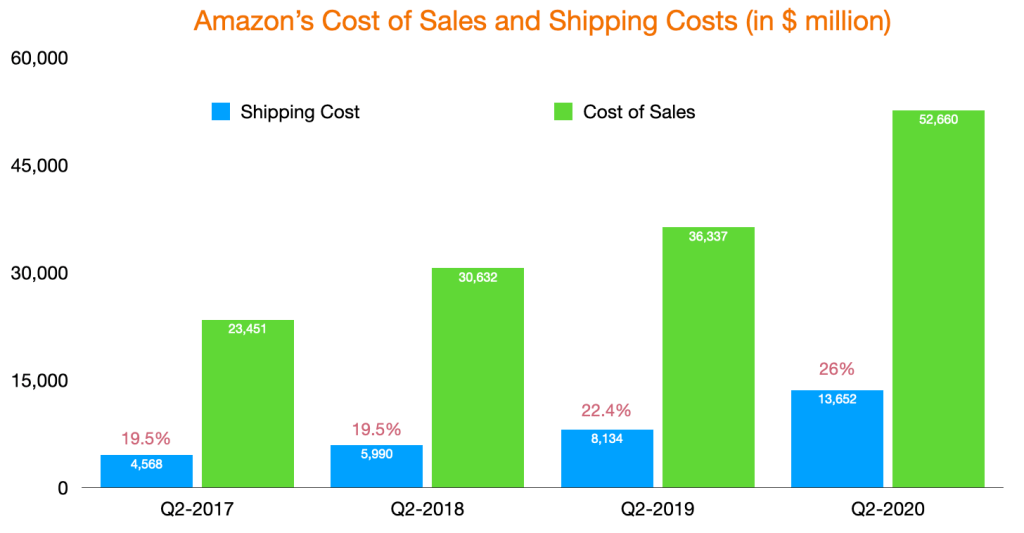

Shipping costs grew to more than $13.6 billion in Q2 FY 2020, from $4.56 billion in Q2 FY 2017. In the last four years, shipping costs rose at a faster pace (44% CAGR) than the combined net sales of online stores and 3rd party (28%). As share of cost of sales, shipping costs accounted for 26% of total cost of sales (AWS’ cost of sales weren’t recorded here), up from 19.5% in Q2 FY 2017. According to Amazon’s 10Q, here is how they define Cost of Sales

Cost of sales primarily consists of the purchase price of consumer products, inbound and outbound shipping costs, including costs related to sortation and delivery centers and where we are the transportation service provider, and digital media content costs where we record revenue gross, including video and music.

Source: Amazon’s Q2 FY 2020 10Q

There are two ways to look at Amazon’s shipping costs in my opinion. First of all, the increase in Q2 FY 2020 is likely due to Covid-19. The rising trend can also come from Amazon’s effort and investment in last-mile delivery which is the most expensive delivery type. Amazon is now the fourth largest delivery service as of May 2020. If other retailers want to compete in terms of delivery, this level of commitment and investment will likely await them. In fact, Figure shows the level of capital expenditure by Amazon over the years. Just. Look. At. The. Growth!

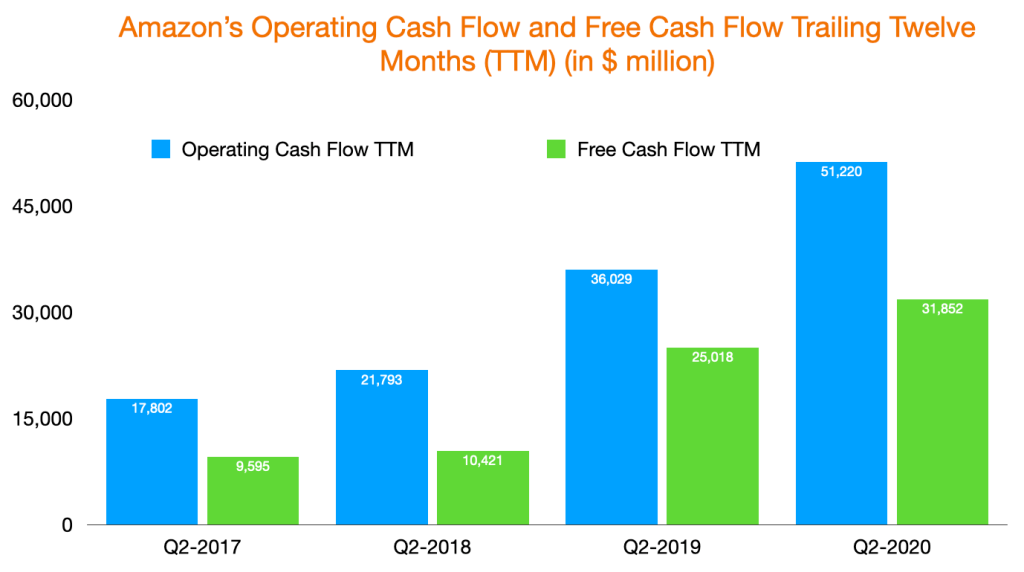

In business, cash is king and Amazon is a phenomenal cash-generating machine. As of Q2 FY 2020, their operating cash flow trailing twelve months (TTM) stood at $51+ billion, up 42% YoY. Free Cash Flow TTM was almost $32 billion.

Additionally, AWS’ momentum is reflected in the remaining performance obligation in the last three years. Performance obligations from contracts whose original terms exceed one year stood at $41 billion as of June 2020, up from $16 billion two years ago. It’s indicative of the revenue in pipeline for AWS.

Lastly, I think this is the first time Amazon broke out their expenses for digital content, including video and music.

The total capitalized costs of video, which is primarily released content, and music as of December 31, 2019 and June 30, 2020 were $5.8 billion and $6.1 billion. Total video and music expense was $1.8 billion and $2.8 billion in Q2 2019 and Q2 2020, and $3.5 billion and $5.2 billion for the six months ended June 30, 2019 and 2020.

Source: Amazon’s Q2 FY 2020 10Q

In summary, I am in awe of Amazon as a well-oiled company. Even at its size, the company seems to have a lot of good things going in their direction and real competitive advantages. The retail and cloud markets are big enough for Amazon to grow more in the future.

Disclaimer: I own Amazon stocks in my personal portfolio.

Leave a comment